Did you watch the film “In time” – where everyone has a clock built into their body and the world economy was based on time – you could earn more time through work and paid with time, and when time ran out you died. Blockchain in principle has now moved this from science fiction to science possibility. The films premise is essentially a form of digital smart contract (the ethereum of the cryptocurrency world) – an unbreakable agreement with consequences digitally encoded in the transaction itself, that can trigger a digital response in another area that cannot be interfered with.

I start with this to deliberately present a distopian world triggered by blockchain technology, as most of what I have read about blockchain paints utopian pictures of what we can do once we rip the technology away from the crypto-currencies of today with their dark web and black market connotations (this origin in itself should be enough to give pause for thought, but apparently not). It is deliberate because most of the examples I come across are pitching blockchain as a utopian disruptive and potentially world changing technology, for example a short list : allowing refugees to own their own identities, rethinking the whole way we build and operate institutions and governments making them much more accountable, enabling individuals finally to have 100% direct control of their own data (genome data, social data…) and eliminating black markets. I don’t know about you but when I read these statements and think about the movie, In Time, it all feels like a very thin line between utopia and distopia and all these examples can easily be flipped given the “wrong owners”, people with high self interest – i.e. a lot of people – and with resources that can be mobilized on large scale. Potential markets for this flip-side distopia are already here today, for example the huge vested interests and money in human trafficking and modern slavery – if they can create even better ways to lock people into impossible situations that force them to work, they will. Why not a smart contracts in blockchains to digitally “hardcode” lockins that mean no work, no access to basics – they may be able to reduce their people costs to look after the “slaves” in the process – then i’m sure they will do it – it might not be directly reducing life but pretty close

The point is simple – blockchain is no different to other technologies and, as we are finding out with social media technologies, can be used for good and bad, regardless of the initial utopian intent. Its the structure and checks and balances we put around the technology that are going to dictate if it creates value or not for all stakeholders – no shortcuts to innovation.

Hopefully I’ll get the time to pull out of draft thoughts on how we can develop the frameworks needed to make blockchains succesful in a business context – but I’ll keep this post short. As always thoughts and comments welcome.

People , once outside their competence, cannot judge how wrong they are ( and usually think they are right – the illusion of knowledge).

People observing groups work, consider groups that change direction (pivot) to solve a challenge as worse performing than groups that set a clear scope and plan and stick to it (when tasks are controlled to have the same outcome and performance regardless of approach).

If, given a multiple choice exam, you pick an answer and then have doubts and think another answer may be right – you have a better chance of being right if you change your answer rather than stick with the first answer.

People have a strong desire to maintain consistency once committed to a direction and behavior.

These are outcomes from investigations into the psychology of behavior of individuals and groups (from work by David Dunning and Justin Kruger and others). Note the text is my paraphrasing.

When I read these insights from psychology – they opened up a lot of questions in my mind about how we work with Innovation and supporting processes like Agile and Lean startup (MVP/Build-measure-learn).

I have always been asked to think about Agile and Lean startup as models how to work with high risk projects or explore new business models ( i.e. processes for accelerating success in innovation).

They are sold as ways to create small , self-motivated teams, who can move fast and ensure the outcome is quickly adapted and changed so we get close to the real customer value as we develop the offering.

When I started to look at the psychology of behavior, this opened up some other thoughts.

Lets look at the insights above:

“People , once outside their competence, cannot judge how wrong they are (the illusion of knowledge)” .

When we start activities with high uncertainty and risk – pretty much the definition of innovation related activities – we (the team) will be operating outside our competence by definition.

From the insight, it also means we will have no idea how wrong we are – but will tend to believe we are better than we are – “Your baby is ugly” is true – and you will not know how ugly it really is.

This means, for Agile and Lean startup processes – the real aim of the process must be to ensure that the team finds out where they have no competence and do something to challenge their knowledge and competence , and then build it up competence to meet the challenge.

The psychology implies something that is obvious, but not something that we often focus on when starting up Agile / Lean startup – we have to build up our competence. Slightly different to finding the customer pain / gain, fill out the business canvas and so on.

How many of you have run innovation processes or agile projects where a team is selected because they are a “talent” team of new high fliers. Or been led down the path that what we need is “new blood” with “new mindset” to bring in innovation.

I have had the privilege of running innovation events and processes with all sorts of mix of teams. There seem to be very little common elements that drive the successful teams, but these two observations seem to hold true consistently (both are needed):

Teams that have at least some members with strong relevant competencies in the domain in question do better (eg. compared to pure talent teams with high general competences)

Teams that are highly reflective to outside inputs, responsive to make changes and effective in using others, do better (ie are effective at building new competences).

The psychology statement suggests that if an agile / lean startup team do not show they can respond to inputs and develop competences , then we should change people within the team. Also teams that have no basis in the problem (have no strong start point in relevant domain competences) are going to struggle and take a lot longer to get going – usually longer than a large organisation has patience for – and should change their team composition.

We forget , perhaps, a bad team is still a bad team, also in Agile or other innovation processes. Team competences, together with a learning mindset, are a critical part of this. The process does not solve this – only (hopefully) makes it more obvious earlier.

Having said that – we can also see why the process structure of Agile and Lean startup variants are powerful, from the psychology point of view.

Both demand that the team work in short cycles where they do something, test it works and demo it – then change their next actions based on observations and learning. This inherently forces teams to quickly test their ideas work and then ask external stakeholders to verify it.

External verification and fact based testing on what you have done is about the only way a team will know “how wrong they are” and if they are on track to “get it right” – and so move from the illusion of knowledge to knowledge – provided they change based on learning.

Essentially, we are , in these processes, building in a countermeasure to a human behavior for the “illusion of knowledge” that works against innovation. This, in turn, suggests why these processes have such a positive impact when applied effectively.

As an aside – we often use the word “customer” to define the group that we need to test / demo with. I think this often leads to confusion and unnecessary debates (“we can’t get the real end customer this time, but Bob will be an OK proxy”). Instead we should use the idea of the most competent “external verifier” we can access, relevant for the question or assumption being explored.

“People observing groups work, consider groups that change direction (pivot) to solve the challenge, as worse performing than groups that set a clear scope and plan and stick to it”

This one, I think, really suggests why a more formulaic process like Agile works in larger organisations as a framework and why Lean startup has great ideas that can be used to replace more rigid process elements of Agile – and not the other way round.

Stakeholders – or the people who pay for projects – really do not like a process that says we can pivot and change as we go and cannot articulate clearly where we will end.

We need to be able to change directions and pivot to overcome the bias of “how wrong we are” and yet our paymasters see this as bad performance – instead asking for things like business plans and clear targets within specific time lines.

Lean Startup thinking is the most articulate and clear on need to pivot and learn and how to manage exploration and high uncertainty – addressing the individual and team bias mentioned above – but does not provide any real crutch of reassurance for stakeholders to invest in the process and feel some element of control in their investment. This is problematic, as its always difficult to change peoples mindsets, and if we don’t provide some kind of structure that helps , then its often down to just persuasion, training and case examples of success – slow processes that are difficult to scale.

Agile , however, manages to convey a sense of direction and provides a structure that paymasters can use to help guide their behavior and helps stakeholders feel like the team is driving in a consistent direction with a plan and purpose. It then, through frequent interaction with stakeholders (eg via demos) – allows them to express concerns and be brought along a journey of the team changing directions in a manageable way (from the stakeholders point of view).

Agile says we have a project vision (clear high level direction) and through its elements like release planning, sprint structure and backlog thinking, allows teams to roughly predict ahead how long things will take without knowing exactly what will happen. If we consider the psychology insight above that observers don’t like teams that change direction, then this is a much more reassuring framework ,psychologically, for stakeholders than one that says we will pivot and change, like lean startup. This suggests that combining the Agile elements that support stakeholders with lean startup elements that are very direct in the change and learn loops could be a strong combination from a psychological viewpoint, to these different key groups.

“If, given a multiple choice exam, you pick an answer and then have doubts and think another answer may be right – you have a better chance of being right if you change your answer rather than stick with the first answer. However, in general, individuals have a strong desire to maintain consistency once committed to a direction and behavior.”

I’ll put the last two statements together. For me, this suggests, as an individual, you have a better chance if you pivot than if you don’t – but our instinct is to stay on the course we have chosen. (Its not quite the conclusion of the psychology trials – but close enough.)

Basically, at the root, we have a mindset that likes to have consistency (and stay within our comfort zone of competence). However, to really deal with innovation and uncertainty, we have to pivot and change based on external inputs and learn as we go.

This means we must train ourselves to manage our bias as individuals not to pivot and change. In this way the principles of both Agile and lean startup are again effective at providing a value set and structure that provides a countermeasure to this bias at an individual level. In particular – both strongly push the bias for fast action and learn rather than planning and analysis.

In summary these statements mean , at the heart of innovation, we have a dilemma of human behavior – we are asked to behave in ways, at the stakeholder, team and individual level, that are not our preference and we are exposed to unconscious biases that work against innovation, like thinking we have it right when we don’t.

Agile and lean startup (and the many derivatives and variants that follow a similar structure) are process frameworks that mitigate the worst elements of human behavior from a psychology point of view and as such are a strong support to innovation – indicating , perhaps, why they can be very effective.

In particular we see there are three key groups of people, who are key in innovation from a behavior viewpoint, that should be addressed by whatever process we decide to use, to help correct for natural bias against innovation. These are:

The individual person, their competence and motivation to engage and learn

The group or team, their motivation to exploit each others competence, engage with each other and external, share goals and jointly learn

The stakeholders or ‘ paymasters’ and their motivation to succeed through the teams results ( typically to earn money / get a return on investment of some kind)

This means that we should be able to merge and modify elements of innovation models & processes freely, provided we retain the key elements that support the preferred behaviors we want in the three groups to support innovation.

An experiment to focus on behavior rather than any specific “process” formula – we did try such an exercise on a technology innovation project.

We kept the structure of time-boxed sprints and demos – for the stakeholders to be able to follow and feel they can effectively express their opinions and be heard. This addressed the stakeholder need for some consistent structure and address their behavior bias against test and pivot. It also provided the team and individuals with some sense of consistency and overall direction – also a key behavior need that was requested by individuals in the team.

Then we focused on using the rapid assumption / testing loops from lean startup “build – measure -learn”, where teams must ,fact-based, verify top uncertainties rapidly with external inputs and objective testing. We also challenged the team to define multiple possible “design directions” to explore in parallel. This ensured a structure to test how much we don’t know quickly, encouraged the team to exploit each others competence and reach outside for external verification as a foundation in all activities. This addressed the “illusion of knowledge” bias outside the teams competence zone and avoided the trap of following one direction too long (avoid the team and individual preference for consistency of direction). Instead driving quick learning loops. It also reassured stakeholders that progress was being made.

Finally we worked with the team for a day, to practice rapid testing loops, getting verification from external sources and then adapting the next tests based on leanings. This training – where people experienced directly and personally, within a training environment – the benefit of rapid learning loops and following multiple options, closing them down quickly – was seen as the best way to address the individual behavior biases. Feedback reflected this – after getting first learning from very rapid tests – it opened eyes how much can be gained quickly. This re-enforced in the individuals that this approach worked, giving confidence to continue in the same way.

In this way, by thinking about the basic behaviors we wanted to support, rather than any specific process, we merged ideas from several sources to get a simple process that was up and running in a few days.

Interestingly – we could not impose co-location or dedication into this project. We instead put some simple , effective virtual tools in place with a time each day the team had to be online working on the tasks.

We also dropped a number of other elements, that are considered key in different processes, but are complex to embed and train (eg strict role definition and splits like Product Owner & scrum master).

So far – it seems to work well – suggesting if we focus specifically on supporting underlying behaviors that drive innovation in the three groupings of people that are key for a project – we can go a long way with simple process structures.

I have both a Dropbox and a Netflix subscription. The one I think about most is Netflix. It’s a fixed monthly fee that I know I can manage if my situation changes – and indeed have done – taking a break from Netflix for a while and using another streaming service, running two in parallel for a while and also canceling both for a while. It fits my mental image of what I think is best about the digital world. Flexible, get to see what I want, when I want – pay for use and stop when I want. But then there is my dropbox account. Maybe running at a 10th of the yearly cost of streaming services or less. However, I have spent a long time making sure dropbox is my safe haven for my family photos and videos. My backup of backups. Now running at family photos dating back to early 2000! Clearly, I could change in theory and it’s a flexible subscription if my circumstances changes. But it’s really a fiction. I won’t be dropping this subscription any time soon. There are too many lock-in points to make this anything but the most painful transition and I sincerely hope that I can always pay this amount and Dropbox does not go on a systematic price increase with me – because I fear I will have to say yes.

This leads me to wonder about what happens if my Dropbox lock-in becomes the dominate situation in the way we pay for our digital economy – particularly from a company perspective. What does this mean? Are companies at risk of creating a debt bubble, locking in uncompetitive cost structures and reducing profitability, as they accelerate their transformation towards the “digital economy”?

These are personal opinions and in no way reflect the situation or opinions of the company I work for.

The trigger for asking myself this question came from a UK Bank of England warning last month that a potential new debt bubble was emerging in the UK around personal debt, with one of the main drivers, this time, not being housing, but Personal Contract Plans for cars – or leasing to you and me.

A long way from the digital economy maybe.

However, my first reaction was to draw a connection – because car leasing – for me – seems a bit like my Netflix account. It gives limited financial exposure, ability to be flexible and walk away after a shorter period, rather than invest in an expensive asset, ability to pay per use (of a sort) with all risks taken care of, ability to change cars (technology) as they change on the market and so on.

Now someone, that I must admit knows a hell of a lot more about these things than I do, was saying something that felt like the opposite to my intuition. Car leasing could lead to more risk. Not less risk. And even a bubble. Clearly this is something to do with penetration – when PCP’s were not the main form of financing, no flags were raised – it is a problem because it is becoming a dominant model to pay for cars. So what’s going on? and can we use this case as a framework to look at what is happening in companies who are moving to a digital model? (which is most companies I know of).

Several elements were raised in the discussions around the Bank of England announcement – all being risks increasing rather than direct problems here and now. So here goes – I will take some elements gleaned from some articles and news items around the UK emerging risk in personal debt, and then attempt to take these over to the world of the digital economy and digital transformation that companies are now undertaking.

From the not so deep reading around the announcement on car leasing leading to personal debt, I have picked up three types of risk.

1) People lock away money into a higher fixed monthly payment, and the flexibility promised becomes a fiction.

Once in this system, a lot of people do not build up the capital to make the down-payments for loans to buy a car and PCPs offer a way to avoid large down-payments. This essentially means people must stay in the leasing system. Flexibility becomes a fiction (people must have a car) and a person becomes committed to a high fixed cost that cannot be varied. At best maybe they can move to lease a smaller car next leasing round.

This is different to when you buy your own car. The financing / debt part is a lower fixed outgoing – often a reasonable down payment is demanded with slightly more credit checks – and a lot of people will reach points during their ownership where they pay it all off and free up the money to other stuff. People are also able to some extent vary the monthly outgoings (and implicitly vary the risks) over time periods. Remember that time you skipped a year of “official services” and went without, or did not follow the garage advise buy new tires or whatever was recommended because it was not urgent. You could vary the commitment without giving up the car. Also, if pressed you could change your monthly outgoings quickly. Maybe sell and buy a similar car but older and with more mileage, using one to put a down payment on the other and cut immediate monthly outgoings.

2) People “over-pay”

The leasing structure encourages that we take the slightly better option – as they buy large numbers in bulk and for specific models / options offer very attractive monthly fees, without the person really feeling how much additional risk is being taken on, for what at the time seems an affordable small increase in fixed monthly outgoing. A big driver to this is that access to money is cheap – so that people are encouraged to do this and finance is almost always given.

3) People are still exposed to market risk – and the risk increases.

Most leasing build in some connection to the market changes to manage risk – in the PCP case it is tied to assumptions that the second-hand market prices for cars do not change a lot. If they change – people in the leasing will have to change their payments or maybe need to find additional money to cover the difference in order move to the next 3-year leasing. The system becomes sensitive, rather than robust, to particular kinds of changes – and often builds in its own pyramid effect and fulfills its own weak point. In this case if all move to leasing, the overall uptake rate for new cars goes up, and for a while drives new car growth. However, at the same time builds up a potential large negative correction of the second-hand car market as the market for these cars is undermined.

I am sure there are different leasing structures that help a little with different risks- but the end result is that a lot of people are locked into a specific form of financing that demands a fixed amount is taken out of people’s finances continuously with no break. These people must have a car, and can end up in a situation they must continue a leasing approach, and if suddenly they need to vary their fixed amount for other reasons, they are unable to. At this point the leasing becomes a personal debt issue and will play out as such in their lives. If everyone does it, and the system becomes very sensitive to specific type of correction (that the system itself will possibly trigger), then it’s a bubble that can burst.

Again, as always, a lot of simplification in this – but I think enough to set a frame to think about digital economy, and companies transitioning to this economy.

So, moving to this area – there are many business models in the digital economy – but that is not the point. The question is, are there any taking over as the dominant form, and does this have some of the same characteristics we see in the Personal Debt case above. If so, are we building up a company fiscal cliff?

If I look around at the business models that seem to be most in use in the company space – there are not a lot. The dominant approach seems to be a modified pay-per-use IT cloud solutions based offering to enable the company to be part of the digital economy -and its everywhere throughout a company. In its IT infrastructure, in its product/service sales systems and even in the actual core product/service offering itself. In terms of infrastructure, process or service, the cost is often tied to number of people using the service (think Salesforce). It might also be products/services a company uses to carry out functions to support for example R&D – or maybe storage space in data centers, then amount of times services are used or quantity used may be the payment metric (think Autodesk world of simulation and other tools with their token system for tool usage), or maybe its supporting sales transactions themselves , for example an e-commerce billing system like Fastspring – then it’s some % charge per sale amount like a credit card cost – often on top of a credit card cost if purchase is with a credit card (so a pay per use on turnover). Now we also see emergence of breakthrough tech. – for example a sensor that for certain types of applications embeds all that’s needed for a company to extend its product to sense more and transport that data to a cloud environment – but these companies are not selling the sensor to other companies as a variable cost direct material component – instead they sell the data cloud info as a pay-per-use / subscription type service and give the sensor as part of the fee.

The payment structures are clearly varied and build in discounts – but it’s likely to be a combination of a monthly base fee + a usage payment model + some enterprise discount as the usage parameter grows. All this looks basically like a kind of leasing set up to me – and one, like the PCP above, that is dominating and growing fast. This, of course, is not surprising as it fits the value selling “Netflix” mental model of what the cloud and internet is about, which is the one I think we naturally carry round in our minds – ensuring flexible “agile” company structure – scalable with use, avoid heavy maintenance, keep updated with latest functionality in the prices and so on.

There are other models like freemium and still a traditional standalone cost then fees to upgrade, as well as companies that basically build their own in-house solutions – but clearly standalone is the “traditional” approach that is being challenged and seems to be losing out. Freemium seems to end up looking like the pay per use type scenario in that any company starts with the free element to play with the system, enabling the seller to get in, then when the company decides to use it systematically they pay the subscription tied to usage – so back to a subscription / usage model. Basically, this for me is like test driving cars before buying – clearly you don’t expect to pay for that. The do-it-yourself model is definitely seen as “not a good idea” ( specialist in-house solutions based on a few experts, heavy unique maintenance , high risk to fail to update at pace needed etc ) unless you are one of the players selling the IT cloud based enterprise system to companies. These guys interestingly, often build their business models up with heavy doses of core open source offerings, or make deals with each other – so are often not tied to the same business and hence financial model as they are selling to the rest of us.

So, let’s try and use the above car leasing as a framework of tests to see if there is an issue in the world of companies moving to digital / Cloud based enterprises. My focus is companies undergoing a transition where they are moving both underlying IT infrastructure and usually also product offerings to be cloud based – often called digitalisation or moving to the cloud based economy. Usually these companies have some strong business model based around selling one-off products and or services – so will have strong focus on Profit & Loss and Balance sheets , typically around turnover, contribution margins, fixed costs, EBIT, CAPEX, Cash Flow and so on.

The first test is – are we locking ourselves into a fixed monthly outgoing that is high AND is the flexibility to change or vary this an illusion?

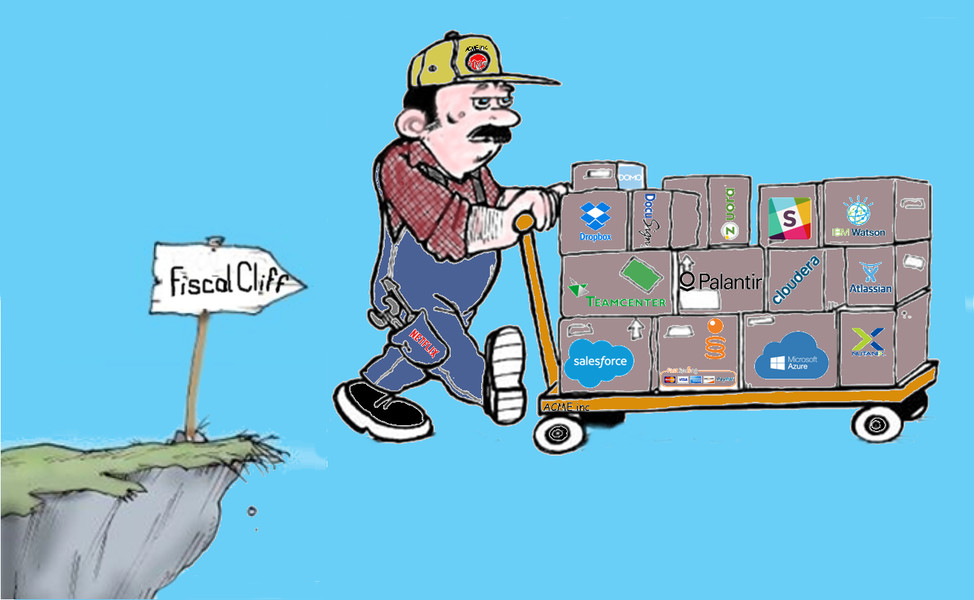

For me personally this is my Netflix subscription vs my dropbox subscription argument. Are companies buying cloud services that lock them in? As far as I can see, in my limited experience, companies play with a lot of these services, but eventually decide for reasons of efficiency, to scale up a few across the company. These immediately are configured to the companies needs and essentially the company locks itself in. It seems like its Dropbox all the way to me. As the picture at the top of the article shows – we are not talking about one or two systems, processes or value add elements, but many packages. Each one seems a reasonable fixed cost to take on board, but quickly they add up to a large fixed cost to the company. Going out every month. So, high fixed costs. I would love to know what company IT budgets look like as the company moves to a cloud based approach, and how much the fixed expenditure on software subscription license jumps – but I am sure it’s a big jump – a bit like moving to leasing. Of course, the total cost argument is used – less people in maintenance and so on – but bottom line – jump in fixed cost outgoings.

The second part of the first test is flexibility. The mitigating idea is that these cloud-based product/services we pay for become more like our direct material variable cost – we gain flexibility as the company situation changes. Here to some extent I agree, but I don’t see this like the variable cost of a product. It’s something like a blended fixed/variable cost that impacts the profit and loss, as well as the balance sheet, tying up cash.

It is tied to usage drivers so eventually there will be a cost reaction as company’s sales and traditional fixed costs (usually people and related costs) change. But the lock-ins are big – discounts are built-in that mean it’s not a linear reaction. There are many different cost drivers built in (as mentioned above), so changes to monthly fees are slow and not immediate and you may have to fall a long way before you can impact the fixed monthly outgoing. It is a tax that is likely spread across turnover, number of people, amount of usage of the service (like storage or simulations) that indirectly and weakly link to changes a company might see in the market. So for example, reducing the workforce will have an impact on usage tied to people – but no guarantee it’s a simple and quick response as only part of total monthly fee ties to people usage as driver and the discount likely means a big headcount reduction is needed to move the needle . All this means slow reaction that probably will be way too little, too late to help any quarterly or even yearly changes in the company’s fortunes. So not totally rigid – but not good.

What about flexibility to change? the car service skipped or buy a cheaper used model idea from car ownership? This also seems not possible. If you have a drop in contribution or drop in profitability or whatever – you’re not going to be able to look to your cloud costs to help you out. There is no time out available on the fixed outgoings and no sell and buy a cheaper model.

In summary to the first “Car Leasing Bubble” test. Yes, to fixed cost outgoings increasing, a pretty weak argument that the outgoings will scale costs up and down over time, based on usage, and Yes to no flexibility in the leasing model itself to “skip a service”. You’re on the hook.

So on to the second test – do we buy too much – or “upgrade” to a car we would normally not buy. Well in terms of the availability of cheap capital – my impression is that if we think that people at an individual level have access to cheap money – that’s nothing compared to what companies with reasonable balance sheets can access. Of course, companies tend to think a lot more about spending money – so tend to be much more careful. However, the cloud based systems we are talking about , for me, seem to be premium product only across the board. The only product available is the one that has all the functions you can think of, so that it can configure to a wide range of industries and applications, so you always are buying a premium package with many features you will never use. In addition the product will usually belong to a family of modules that you are also encouraged to buy. Result seems to be we always pay for the trade up model. So the second test also seems to indicate a problem.

Lastly does this cost model and all these many systems we are now paying monthly fees to, expose us to a greater market risk, or even worse actually help accelerate the risk. This is clearly not so simple to answer as the car leasing situation.

One risk is clear at the company level, and that is companies are tied to a high monthly outgoing that is not so flexible. This exposes companies to rigidity rather than flexibility in their cost structure, making them less, not more, able to adjust as their fortunes vary in the market. This will be amplified if the company business is around one-off sales and is transitioning – as it has no financial language or performance systems to offset this increasing fixed outgoings against normal quarterly variations in the markets and the resulting variations in margins, and other targets it sets itself.

Another risk that is at a market level, is bankruptcy of the IT enterprise system supplier. This will happen to some. Given the fact that many of these systems end up being like my Dropbox – this becomes a company critical issue to the companies using the system. A clear warning trend for this risk will be that especially larger companies will go for vendors that are “too big to fail”. Like Microsoft or Salesforce or SAP, escalating the problem of tying a huge percentage of larger companies in the hands of a few platform players. This is because of my Dropbox effect – second sourcing or similar tactics that are the mainstay of risk mitigation by purchasing are no longer possible. Clearly this consolidation effect does build up a potential for a bubble – in that shocks to a few key vendor players can have an over proportional effect on companies. For example, sudden jump in costs charged by a vendor in trouble would impact profitability and cash flow disproportionately across many industries, as would a bankruptcy of one of these big players – that would be like a mini bubble bursting, rippling across different industry segments. Is this likely? It’s certainly possible, so in that sense, there is a market risk that increases as this financial model is deployed, building in a bubble. It doesn’t seem very likely though – the big players, although have accelerated fast into the markets – seem very resilient so far. And in the enterprise space, if new technology disruptions occur like the current Salesforce and other vendors of cloud-based CRM taking over traditional CRM suppliers – they occur slowly and it becomes more a lifecycle adoption problem that companies plan for and manage (even if very painful).

What does seem likely is that companies will find themselves in a much more rigid cost structure than they are used to – locking in a cost to do business. In non-volatile conditions, it should work – companies will clearly drive productivity and efficiency savings to make up for the additional cost. But it does open questions about competitiveness and ability to handle volatility in a financial sense. It will be harder for companies to make corrections – they will have to cut deeper into their workforce or other costs to compensate for market changes than they are used to, they will have less control over contribution margins, profits and cash. Winners will be those that integrate and utilize the new functionality and cloud environment best – but that means those that integrate the systems and make them part of their business model best – paradoxically make them more dependent, not less.

So overall – maybe not a fiscal cliff – but it is a steep path next to a drop of some sort. It seems we have a period now of many companies adopting the same approach. So there is a risk of a dominant model for financing digitalisation emerging, as as concluded above, it does seem to share many characteristics that are common with a sector financial risk bubble.

As a result, we could be in for a period of relatively high cost structures despite acceleration of automation through AI, machine learning, robotics (both SW and physical robots) etc., so we end up with this strange effect of less jobs, seemingly increasing productivity in the companies, but no real outward impact on competitiveness, prices and so on.

Note , this is a review only of the financial model dominant around digital / Cloud IoT, not of the technologies themselves. I do not advocate we do not digitalize, or even slow down. However, we may need to think carefully about transition strategy – and what options and alternatives we have.

There are alternative strategies companies could take – I outlined one at end of “How do companies compete when Industry 4.0 hits?”

I would , as always , love to hear your comments and thoughts , if you get this far

“Innovation occurs when there is external confirmation that a value aspiration gap has been reduced”

This definition of innovation came out of a forum discussion between myself and Don DeLauder, as a response to a question by Eugene Ivanov. I started with the intention of arguing that defining Innovation was a pointless exercise and ended up writing a definition that was thought provoking for me – hence the decision to share it.

First let me unpack the definition a little.

A value aspiration gap: This is a value gap that is opened when a tension emerges between the current state and the aspirations of people and/or entities. This is sometimes referred to as “unmet needs” – but innovation can be wider that just “needs”. If this tension grows it creates an opportunity and if people cannot find a way to close this gap with what is available in the current state, then some form of innovation is needed to fill the gap. In other words the need for innovation comes when the status quo fails to generate results that meet our aspirations, whether now or in some predicted future. In that case we need to create more value-we need to innovate.

External confirmation: This is when someone or something external to the creator / inventor confirms that a value aspiration gap has been reduced (ie some aspiration has been all or in part met) by assigning recognizable value to the innovation.

This idea that innovation occurs when we have confirmation external to the creator / inventor is broad – so here is an attempt to place some “boundary markers” . The idea being if one marker is crossed – it may be innovation – but as more are crossed , the certainty that we are looking at innovation goes up:

a) Confirmation of Financial value has been assigned to the innovation by a user – this could be anything from a third party willingness to donate in kind, to more traditional payment

b) Availability (the creation is available / accessible to others)

c) Shown to have addressed a real value gap – ie other people are using it to do something they did not do before.

d) Recognised by independent sources as creating value (eg technical magazines, reviews, trade fairs and the like)

So lets take this definition with the above clarification and run some thought experiments to test the definition in action.

Innovation covers a lot of ground often expressed in terms of “incremental” or “disruptive” – and everything inbetween. A definition needs to be something others can apply and use as a filter to say what is , and what is not , innovation. For our thought experiment – we need to try and identify things that could be innovation, then see if the definition helps show if they are inside or outside the boundaries of what is innovation, as set up by the definition.

To do this , three examples are picked for the thought experiment (coming from the discussion mentioned above).

At one end we can take the birth of quantum theory – here I am thinking of Einsteins theory that won him the nobel prize. In the middle , lets place Betamax – the innovation that lost to VHS (before both were overtaken by DVD , BlueRay and now streaming). At the other end we place any invention that failed.

If we take quantum theory – clearly this has been the foundation that has led to many breakthrough technologies like Semiconductors, in turn leading to things like strained quantum well lasers and then to CD players and the like. However – this fails to show a value aspiration gap. It takes time from theory breakthrough, to people , to understanding and interpreting , to new technologies , and during this , people start to develop aspirations for things that were impossible to imagine at the time of the breakthrough , creating value aspiration gaps – and then innovations start to occur to close these gaps. So in itself the theory is not innovation, but clearly the birthplace of much of our modern world. Innovation occurs later.

The failed invention loses out because , although the inventor has percieved some value aspiration gap – there fails to be any external confirmation that this is a real gap – so it is a “wannabe” innovation – but by the definition is not innovation.

Finally Betamax. This cleary fits the definition. People bought it , it was recognised as innovative, it was used and so on – all the indicators of external confirmation being met. Betamax failed due to normal business dynamics – in my simple version, both closed a value aspiration gap, but VHS got a better handle on the real value aspiration gap (wide content selection with good enough technology) so won the business battle over time.

The outcome of the thought experiment “feels right” – ie it successfully and clearly separates what is and what is not innovation in a way that, although utilitarian, seems to work and give meaningful answers. So its a good working definition. The boundary markers can, I am sure, be improved, but they seem also to work.

One interesting thing about this definition is that there are no words in the definition that states an innovation must be something “new” or “created”. These are two words often used when trying to define innovation, but make a sharp definition very difficult.

As long as the value aspiration gap is reduced, we have innovation. Creation is implied but not needed as part of the definition. Newness also is implied as an outcome, but not needed. It becomes instead a property people can assign as an outcome – things are percieved as new if they close a value aspiration gap – but perhaps are not new in some other context.

I hope you find this definition also of some use. Comments always welcome.

I wrote this a while ago (2016 I think, maybe earlier) – and its being sitting in draft doing nothing. I thought it time to put it out there. Have added a few comments to make it seem like it was written recently…enjoy

I have been subjected, like many of you I suspect, to Apple being used as the pinnacle of innovation in many a business conversation – usually with someone (internal and external to the company) trying to convince me that what we do today is inadequate and if we just did “x” , then we would be much more innovative , profitable and experience exponential growth “like Apple” (used to imply we are hopelessly behind, and its obvious what Apple is doing that we are not – but with little further detail). This has thankfully died down since Cook took over – but still is brought out now and again.

Like many people , I have been an Apple watcher over the years, and formed my view of Apple between 2001 to 2010 (iPod launch to iPad launch in “Apple Time”) – and it has not really changed since then. I am sure this point of view has been expressed – but I actually have never heard it – and yet another Apple talk by someone recently got me thinking I might as well add my version to the 1000’s already out there.

Apple to me is a company that has truly mastered Technology Management, Product management, Product development, Supply chain integration and above all launch disciplines , combined with a unique attention to detail in customer experience. All being traditional disciplines and not much to do with the type of innovation, implied in the introduction, people sell me about Apple.

My first realisation of this was when I bought the first iTouch – for those of you who have forgotten – it was released as a touch screen version of the iPod – with no apps store and no bluetooth. I then listened to Steve Jobs, in one of his live streamed events (at that time you needed to download the event), announce the Apps Store , and that everyone who had an iTouch could upgrade to the Apps store for an amazing discount rate of $25 (or something like this). I happily paid like others and was amazed at how little backlash there was to this charge. A little later he did the same for the launch of the next OS X and charged something like $50 to those that had to upgrade. Again little backlash.

I started to pay more attention to the product releases coming out of Apple. The lack of bluetooth at a time was completely against the de-facto rules of launch , as it was standard with competitors, yet still the iTouch was smash hit and with very little backlash from consumers (or non really I could determine at the time, except by reviewers). Then the perfect positioning of the iPhone on stage as a 3-in-1 device (phone, internet, music/messaging — the third always got a bit grey). Then the positioning of the iPad as the missing piece in our lives with iPod/itouch/iPhone at one end of the mobile spectrum and the Apple Air / Mac at the other and the blatantly obvious (when Steve showed us) gaping market hole between the two just waiting for the iPad / mini iPad to fill.

Each of these events were announced in advance on stage – with prices! I still consider that series of live stream events a better education in product strategy, product positioning, launch strategy and pricing strategy than anything in a text book. If you can find it – just look at the stage performance where Steve Jobs launches the iPad. The perfect start by redefining the product category of mobile devices – the perfect identification of a missing product position within that category (the iPad) and then perfect delivery into that gap. Why bother with text books or executive MBA – as an educational video on how to do product strategy, product positioning, value propositions and product pricing – I have never seen better.

Looking a little beyond these headline events – what does this show us? Well – to launch the itouch , then enable an upgrade to apps and next gen. OS X shows us that this was a product platform with these steps already designed in at the start. The same with iPhones and the upgrades that followed. To do this is not the sign of a company developing an MVP (Minimum variable Product – the textbook expectation of highly innovative companies developing business models and pivoting). Rather it is a development process and product that has been carefully thought through not just for first launch , but also for subsequent product releases.

This thought was re-inforced when meeting a US californian based consultant with insight to product development at Apple. He commented that at an early gate (note gate – so traditional set up) , the project team had to not only outline the product concept , but also the next (2 – 6?) releases that would come from that product family. In addition to this, there would often be parallel teams working on the same product or product sub-system – ensuring competition to drive innovation. Great for those companies with the money to do this.

Then there are the launches. The stage performances are used to announce world wide launches – but typically with US or a limited set of countries getting first release. Often other countries not even given a date at first. As the launch started , other dates would be announced for other countries. In terms of supply chain , I always thought this was a great way to manage the demand curve – so consumers are not disappointed and have a sense of the product being released all at once, but the supply chain using country roll out dates to control the demand curve , so it had a lever to pull to enable factory output to follow demand without significant customer backlash against product delays – Again that ability to manage customers feelings towards the company. Although even this has challenges if the demand is explosive against prediction, like the iPhoneX.

Then there is the complexity management. The apple product range is a supply chain wet dream with tight control of variants, only minimum variants available and a standard , incredibly disciplined and effective phase out (launch a new version – keep only the low end version of the old version – discontinue the others immediately to ensure a hard change over). Ensuring amazing scale with few variants. I don’t know how many SKU’s there are of the iPhone, but it can’t be much more than 100 – a number most companies would die for , in a product group. It also effectively allows new platforms of a product to be launched with low re-use from old platforms (so large room for manoeuvre to introduce completely new technologies, processes etc) but maintain supply chain scale and simplicity (and thereby cost that others can only achieve with partial platform upgrades, stretching lifetime of modules to keep costs low).

Finally the technology mastery. In each area – there is no doubt Apple has identified key technology leadership targets and invests heavily in them. Unlike many companies , it clearly believes process technology leadership is as important as product technology – with each product launch seeming to bring technology jumps in production areas it believes enhances its customer differentiators (like the single block Alu bodies, to the fused screens and so on). This selection of key technologies to lead is clearly also seen in the product technologies applied. And of course – they build this into the promotion – name another Company that will split its technology and show the insides in promotion videos? Not so many on my list – except maybe high end Swiss Watch makers.

All of this , for me, implies a company with an incredible discipline in technology management, product strategy , product development , go to market and supply chain excellence – not a company pushing innovation fast , at the limits , with a series on MVPs and rapid iterations, exploring uncertainties and business models. It implies a company that takes the integrated product development disciplines to the limit – fantastic product platform thinking infusing all steps, amazing product strategy built on customer insight – out of this world technology roadmap thinking tied to product strategy and customer insight – far thinking product development discipline with competition built in and supply chain and market launch completely in sync.

The magic for me is of course the same as all others point out – spotting new “mega” categories from the customer insight (however this is arrived at). This implies a user oriented culture deeply embedded in top management (or I guess most people would say in Steve Jobs personally – but not so sure), as well as in the organisation.

But from this point in – it is just out of the world execution and top management “ice in the stomach” (to use a Danish expression) to follow through convictions. I am sure Apple did its fact finding and saw that customers at that year (launch of the iTouch) – were not so bothered about bluetooth. They , I am sure, like all others , saw it was coming fast, and others would and did include it. But they also knew that it was not yet a key differentiator – so were willing to cut it from the development of the early versions – saving time , cost and speeding up development I am sure – knowing they would add it to the platform next year. To keep this discipline , plan to release the updates and do it, and then repeat it consistently every year- coordinating market, product development , supply chain and sales so seemlessy (from the outside) – using systems like country release delays to manage uncertainty – is truly impressive.

Similarly for the apps store addition to the iTouch. I am sure they were in the middle of apps store development , but could see they had enough differentiators to launch an iTouch without the store, with huge success. So instead of waiting , did that – cashed in – always making sure to ask for payment where they can see they have a unique differentiation to offer. Then cash in when they have the app store (another extra payment for those with older iTouchs) and cash in on upgrades and again in on OS X. They don’t charge when they can see the differentiation is not sufficient to ensure customers are more than happy to pay – so their pricing discipline again seems to be a refined science routed in customer insight.

All of this for me indicated a product Development, marketing and supply chain excellence company that is world class. It does not come over at all as an innovation company with Google like “20% – do what you want” innovation processes or anything like that. In fact all the elements seem very traditional management disciplines in one sense – but taken to a competence level rarely seen.

Then of course Apple adds one more layer. The almost obsessive attention to detail of customer experience at every level is close to unique. All tech Companies clearly now focus on user design, but where as I always feel places like Google do it case by case, for each product – then stitch it together – Apple seems to be able to embed the ecosystem experience deeply into the individual product experience. Clearly with advantages and disadvantages – I would not be surprised that this overall experience thinking means they did not see as clearly as say Amazon, the one trick Echo dot like activating music with voice – even with Siri being around forever.

I always remember the complete shock at the apple map launch failure. In itself it was not really that much of an issue – but to see apple slip in what seemed to have been over 10 years of launches with complete 100% attention to customer experience that never missed the mark – then have them make such a customer experience error – seemed just wrong. There have been other launch failures – but not with such a clear miss on customer experience.

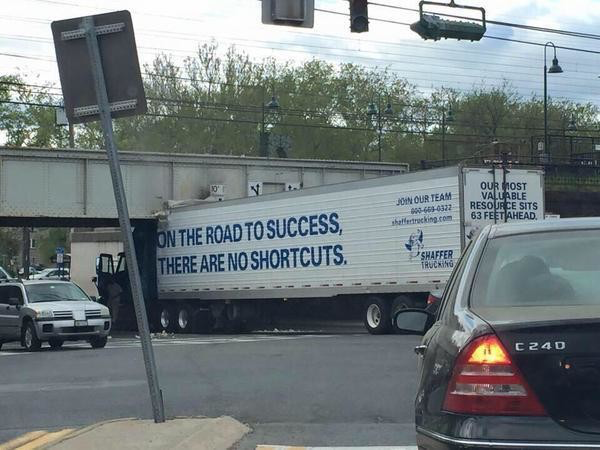

So innovative or business excellence at its best? One thing is “there are no shortcuts on the road to success” seems to be true of Apple – there seems a hell of a lot of hard work , discipline and process excellence going on behind its “innovation success”. Maybe like the saying “chances seem to come more often to those that work hard” , we could say that “innovation seems to come more often to those that drive for customer experience and business execution excellence”

These views are my own and not related in any way to the company I work for.

(Thought I would do something a little light-hearted , maybe slightly satirical. Apart from the line in italics – that I added to list where the 4 congresswomen come from, everything below are verbatim texts clips from tweets or speech transcripts, with some license in how they are clipped and arranged. Could make an interesting rap. All views expressed are strictly personal only)

Bronx, New York. Minneapolis, Minnesota. Detroit, Michigan. Cincinnati, Ohio. Congresswomen. These places need your help badly.

Bronx, New York. Minneapolis, Minnesota. Detroit, Michigan. Cincinnati, Ohio. The worst, most corrupt and inept anywhere in the world. Go. Fix the totally broken and crime infested places.

The White House is running beautifully. I have chosen one of the truly great business leaders of the world to be Secretary of State. He was dumb as a rock and I couldn’t get rid of him fast enough.

Problem is we don’t have stars anymore — except your President. My two greatest assets have been mental stability and being, like, really smart. Sorry losers and haters, but my I.Q. is one of the highest. Please don’t feel so stupid or insecure, it’s not your fault.

No candidate offers USA the honor Donald offers. Any negative polls are fake news. I won the popular vote if you deduct the millions of people who voted illegally. If the totally corrupt media was less corrupt, I would be up by 15 points.

If I build a steel wall rather than a concrete wall it will actually be stronger than concrete, steel is stronger than concrete ok, steel is stronger than concrete, it will actually be stronger. Listen – you can’t really see through a concrete wall, it will be a more beautiful wall than having a concrete wall, if you want a see through wall. I think people will like that. Any money spent will be payed back by Mexico.

It’s freezing and snowing in New York, we need global warming.

When your already 500 billion dollars down, you can’t lose.

Are you allowed to impeach a president for gross incompetence?

The decision was not a good one. The best horse did not win – not even close…

Future markets will be a combination of “dollar” and “non dollar” markets. Industry 4.0 / digitalization will lead to “dollar” markets shrinking but total markets, “dollar” + “non dollar” growing. Basically this is a sum of the last 2 blogs. .The final piece for me in this 3 part story is what happens to industrial companies and how will they thrive and compete – if Industry 4.0 is just going to accelerate the shrinking of “dollar” markets.

The answer for me is that value chains (the collections of customers and suppliers that form partnerships to compete) need to also to blend “dollar” and “non dollar” methods to supply goods and services to meet customer needs, reflecting the new reality of digital markets.

To explore and test this, I will set up a thought experiment to sum up the ideas about how the “dollar” markets will change due to digitalization, and then consider how we can blend “dollar” and “non dollar” in the supply as well as customer side. This thought experiment is ultra simplified to make a point, but could easily be scaled up to a complex model.

Consider a more traditional global setup of some market segment before widespread digitalisation. We will just think of two large regions far apart from each other ( Region 1 and Region 2). In each region, a Value Chain has emerged of linked producers to provide offerings to regional customer needs (Value chain 1 for Region 1 and Value chain 2 for Region 2). Its a global world, so some of the offerings from Value Chain 1 go to Region 2 and visa versa.

Scenario 1:

Global customer demand:

Region 1 | Region 2 | Total

Customer needs: 10 | 10 | 20

Of which are

shared: ° — 5 — ° | 5

of which are

Unique: 5 | 5 | 10

In all 15 unique needs

Global production :

Value chain 1 Value chain 2

Number of offerings: 10 | 10 | 20

From other

value chain: ° — 3 —-° | 3

Of which are

unique 7 | 7 | 14

In all 17 unique offerings

Scenario 2: Along comes digitalization:

Number of customer

needs fulfilled

Region 1 | Region 2

Unique needs

fulfilled: 4 (of 5) | 3 (of 5)

Shared needs

fulfilled: ° — 5 — °

Platform offerings |—-12.—–I

Value chain 1 | Value chain 2

Value chain

offerings: 6 | 6

Custom made

offerings; 1

Needs not met: 1 | 1 (2 needs not met)

So what has happened ?

First – and this is a key part of any digitalization of a market – global “accessible” choice has increased . In the first scenario, there were 10 offerings on the market in each region . In the second there are 12. The platform dynamic of digitalization kicks in.

Next- the hidden downside outlined in the first blog – customers cannot fulfil all their needs as global “total” choice reduces. 3 needs cannot be met by the platform offerings. One is custom made (value justifies the increase in cost ) but 2 are withdrawn from the market. This is the effect mentioned in the first blog where companies can no longer cross subsidize offerings, so they take offering off the market – as cross-subsidized offerings option is stripped away due to the ability of digitalization to ensure customers just pay for that part they want.

As a result – finally – the dollar market offerings (and hence the “dollar” market itself) have shrunk as need and production become transparent. Each value chain has gone from 10 offerings each to 6 offerings each. Almost certainly due to higher competition and emerging transparency eliminating any offerings that are subsidized by other offerings.

Now nature (and markets) abhor a vacuum so something has to happen to meet the needs of customers – in reality they will not go unmet as illustrated in the model. The model is incomplete and something else must happen to allow needs to be met, even if value chains cannot afford to.

First a recap : Industy 4.0 will just make things worse – it is the enabler to shrinking “dollar” markets. Value chains will start by digital-enabled accelerated optimization of production and development – agile product development with increased software and simulation, additive manufacturing and other fast prototyping, fast Development and flexible manufacturing Technologies – leaner supply chains emerge to deliver only whats wanted – “pay as you use” efficient cloud based IT infrastructure will be even more widespread as flexibility at “efficient cost” spreads and companies need to transfer the “pay only for what I want” customer demand through the supply chain so we have “scale cost one to one to what is payed for” – automation of white collar and blue collar work accelerates with cheaper hyper flexible automation among others – “digital factories” emerge in all their possible forms – so factories are more & more decoupled from any particular design needing to be produced , and so on with all the drivers and buzz words around Industry 4.0. All these initiatives just accelerate the digitalization of the total market and shrink market size (for “dollar” part of markets).

All this implies a downward spiral on the value chains that in turn deprive customers at a total market level of fufilling needs whilst they are being drowned in choice driven by global platforms.

However, previously, we suggested we will move to a situation where the total market would be a “dollar market” + a “non dollar” market. Customers will access value by combining both markets, so the “dollar market” could shrink but total (dollar + non dollar) market could still grow. Customers will not be limited to paying the value chain – they can access sharing economy solutions – maybe also carve out and access only part of the value chain and do the rest themselves – or other options opened up via full digitalization.

This same dynamic, however, is also available to industrial companies (after all one persons supplier is another persons customer and value chains are just collections of customers and suppliers that form partnerships to compete with other value chains )

This leads to an obvious answer in how will we compete when Industry 4.0 hits: value chains need to also be made up of dollar and non dollar means of production as they transition via Industry 4.0 to a digital world.

So how does dollar & non dollar blended means of production work?

Today we are already seeing some elements emerging, building on business models that have been part of the Internet subculture (like the open source movement) since its birth.

We have seen the fruits of this social / sharing economy subculture moving into industry, with for example, open source being a part of the corporate infrastructure (eg think apache servers). We also have “old” stories from corporate business of how sharing economies could work for large investments / capital expenditure (as opposed to end user sharing of their personal investments like cars or houses), such as corporate jets being shared between Customers (Netjet).

From this we start to see new patterns. Cloud platform houses that serve large companies are building open source into their offerings, releasing more code to open source and developing and changing their offerings by combining own development with shared and open source development – building customers into the development requests and outputs, much like open source. An example of this is microsoft Azure platform with 1000’s (ok maybe 100’s) of tools accessible – many being open source and much of the code also released – and the development also run in an agile and ”open source” like way with customers. Not sure if it will be successful but its a serious attempt to blend dollar & non-dollar markets and if they reflect this blend in price & value of offering, it could work. It certainly is a very fast dynamic platform – at odds perhaps with Microsoft traditional corporate image.

Another example is emergence of ventures trying to offer capacity on 3D printers to others and I’m sure many other types of industrial asset sharing ventures will follow (another prediction – don’t forget to allocate a fractional value of your company shares to me if this idea is new to you and you start up a venture from it) – so a company can share the cost of invested capital by sharing capacity.

As we move to “digital” products (discussed before) and Industry 4.0 technologies , this type of industrial sharing will become easier and be more and more frequent. We can see with the emergence of shared 3D printing capacity ideas (additive manufacturing) , the key is to solve guarantees of data security – but this is already happening. Then companies can offer, for example, “shared” spare capacity in the same way we share car capacity in say “Go More” or houses in “Airbnb”. This capability to share will be accelerated by Industry 4.0 trends that have a tendency to move the value to the digital part of production and design.

This sharing can easily be extended. As manufacturing designs become digital, it is easy to see that some design templates will become public, others may be available in some kind of libraries at significantly lower prices. Companies wanting to meet customer needs, but needing to keep profit and margins, could start blending offerings – combining their own designs and using their manufacturing capacity and supply chains to also make “free” or shared designs to enable wider offerings – or using their assets to make products for other value chains. We see the release of IP from Tesla playing directly into this arena. We also see libraries appearing on the internet for devices that can be created for 3D printing – its not hard to imagine these designs also encompassing more industrial areas rather than fun things for the home – a quick scan of some of the serious enthusiast areas shows this is not a long way from this (browse thingiverse or grabcad if you want)

So what will we compete on in the future?

In the digital future, customers will be able to get their products from multiple supply chains with help of platforms to get best cost. However, some companies and value chains will be a much better “experience” than others – they will claim higher “non dollar” value through ratings, reputation and other social/shared currencies – and these will become key to success – both for their financial credibility in the “dollar” world and success overall. The future will go to those that compete in both “dollar” and “non dollar” economies.

This will require excellence in two arenas. First, those that can blend the two worlds into their value chains to ensure the correct blend of own offerings with own value add, combined with shared/free offerings of the “non dollar” market to ensure the best value to cost possible. Second those that can create experiences to transfer this value to customers and achieve highest social / shared economy Capital.

Or when are our Internet platform powerhouses like Google, facebook, Airbnb, Uber, twitter , Amazon, Trip advisor going to become our new financial industry giants of the “non dollar” economy?

As a result, going forward we will view markets and market size as a sum of “dollar” and “non dollar” markets.

Previously , I outlined a picture of how Industry 4.0 will shrink “dollar” markets – although “non dollar” value will emerge and to some extent fill this gap. For shorthand – I’ll call the world of money the “dollar” markets or ” dollar” world and the social / sharing world the “non dollar” markets or “non dollar” world.

This time I want to explore this “non dollar” value and “the new gangs of the digital era” that control it. As a result, I will push the idea that these are the start of a new type of financial industry that will emerge to support the “non dollar” markets. (By “new gangs” I mean internet platform powerhouses like Amazon, Google,Tripadvisor , Facebook and so on).

A warning though – this blog is longer and more speculative than the last.

These new gangs of the digital era give access to , and control, the new currencies of the digital age , the currencies of “social” and “sharing” economies ( reputation, followers, likes , ratings, reviews , ..), as effectively as the financial industry control & gives access to money in markets today. Both financial Institutions & these “new gangs” , on the whole, do not directly make the things we want and need , but without them , their platforms & related services , we cannot operate & do our business in the non dollar or dollar markets.

As we begin to place real value on the social & sharing economies emerging in the digital world – the roles the platforms play , it seems to me , look more & more like the roles of financial institutions. Hence the phrase “new gangs of the digital world” taking their cut and charging protection money – a slightly biased view of the financial sector living off others wealth creation work. I understand the argument that these are also essential enablers to wealth creation – but I’ll stick to my metaphor for now.

It is perhaps too early to confirm that we are seeing the emergence of a parallel financial market infrastructure for the digital world, supporting the “non dollar” markets, but we can build up a hypothesis based on analogies to the “dollar” world and use these to predict trends in the “non dollar” world. If we see these trends, then it goes a long way to support the prediction that going forward we will need to view markets and market size as a sum of “dollar” and “non dollar” markets.

If we go back to the USA before the greenback we know today existed ( the story of USA currency before the greenback taken from NPR, Planet Money podcast #421) -we had banks in each city or region issueing their own dollar notes – each note having different relative values in shops based on factors such as how close to the bank you were, the percieved reputation of the bank and so on. Think, for example, of different reviews in different platforms – do you trust the review of a hotel in some web travel site you have never heard of, or do you trust the overall review status af Tripadvisor. It might be that the website review is completely trustworthy to some group of people, but you still discount it in your head – in the same way a shop would discount a dollar from an unknown bank – and for similar reasons – you have no basis on which to place that trust and so you don’t .

Today we are seeing an emergence of agreement or at least “customs” about how to handle things like reputation , likes , reviews and so on. When we see a review or a trending rank for example , we have a picture in our head what this means eg. a review rating is , if in a 5 star format, the aggregation of many peoples opinions who are genuine users of the goods or service in question , and who are not connected to the seller in any way. There is no place where this is written down as the law , but platforms offering reviews converge towards this, as the “custom” is established, and people place their trust in that custom . And those places we think follow best this custom and have scale of numbers (lots of reviews, with well regulated process, as perceived for Amazon or Tripadvisor ) get our highest trust. (This, as an aside, is also close to the explanation why we put value on Money at the end of the day – NPR Planet Money #423). All this is very similar to how a shop would trust a large well financed bank with many customers that is nearby, over one they did not know very well.

To see the power of these customs , it is interesting to see how Facebook makes world news when it is revealed that their ranked trending information is subject to editorial oversight and is not pure trend data . It probably makes sense they should do this , but it is not what we thought was “Custom” so it becomes news , reflecting our unease , even if, as far as I know, no one at all thinks Facebook has manipulated any information in a “bad” way. But maybe they could, and thats enough to undermine a little of our trust.

Back to banks of old- after a while there was the emergence of conversion books as travel & trade grew. How can one shop value a dollar from a particular bank it had never heard of – books were published to help this – complex tables based on how far the bank was , away, reputation and so on. Essentially this was a formalization of informal rules and customs, shops were using to judge the value of a dollar, to enable conversion between different Institutes offering the dollar. We are seeing first attempts of formalised “books” now in some “non dollar” currencies – in particular reputation reviews. Some are trying to build sites that can take reputation from different platforms – attempting to enable people to transfer reputation. Its hard to see these first attempts working, partly I think due to the value of the non dollar currencies in question are not yet trustworthy or consistent enough, and partly because the internet is a place of monopolies, and if 90% of all banking is in one bank (think Tripadvisor) – you don’t need to bother with conversion books. But this is changing, so expect to see more attempts going forward.

So what is down the line ? I don’t think one replaces the other – we will operate with both dollar & non dollar currencies although conversion between the two is not obvious at this time. I am sure some will occur eg I can see ”reviews” and some types of “rating” having some conversion behaviour as they are discrete (ie separate from the object being reviewed and rated) a bit like discrete money units, but its hard to see how you can convert for example , reputation & then reduce your own reputation as a result of “selling” reputation. However, its not so hard to see a trade & markets where different types of “non dollar” exist together with “dollar” & also not hard to see that “value” in the eyes of customers can be a sum of “dollar”& “non dollar” values.

So to predictions

Formalization of trading rules & legal frameworks to handle disputes & reduce “fake currency “. This seems one direction for “non dollar” markets. Already now, we can forge identities & personalities, we can create false follows or false hits to make sure we have presence in a particular “non dollar ” market (think manipulating to push up a google search ranking or fake follows to be impressive on Twitter ). Also people or companies that are deliberately attacked to ensure “bad reputation” or “bad reviews”.. Or the company itself can manipulate its own system. These things are beginning to have significant real word value and financial consequences. In AirBnB , we have two way reputation, so unless you have a history, some rooms will not let you book them, a top Tripadvisor restaurant can have huge increase in bookings, and so on. Today we are at the mercy of the platform company and how it decides to police its own world. When change occurs – it is mass public outcry that forces the platform to take action (think Facebook “panic button” in UK). But today , essentially the platform company decides and no arbitration. Its hard to see this as sustainable, people will demand more fair rules and independent arbitration , as in financial markets. We already see the start of establishment & legal reaction, with for example UK Competition & Market authority investigation into fake reviews in Tripadvisor and Amazon, and with different legislation at local level impacting AirBnB and Uber (eg New York conflict with AirBnB, Uber and Austin).

Emergence of “standard” currencies.The greenbacks & Euro’s of social & sharing economies. Today a review in one platform can be completely different than from another, in the way the review is done (subjective opinion from third party, paid opinion, advertising designed as review and so on). Linked to reviews are ratings. Ratings are more & more valuable – we rate restaurants on Trip advisor. We trust those ratings as honest – now Trip advisor can issue “badges of excellence” and restaurants can then display these in their promotions . But not all ratings are equal. Try giving a bad review on “Trust pilot” – a company that provides ratings to help reassure people if a website is reliable – especially for making purchases. Here the company rules are different and they reserve the right to delete the review if it is not provable to their satisfaction – higher quality ratings? or serving the interest of the companies paying to use Trust pilot. Not sure , but hey, the company can decide its own rules, so whats the problem?.